Volatility: An investor survival guide

Financial markets can be subject to periods of event-related volatility during which investor confidence can be significantly undermined. Here, we provide 10 key messages to help investors steer their portfolios through volatile times.

1. Volatility is a normal part of long-term investing

From time to time, there is inevitably volatility in stock markets as investors react nervously to changes in the economic, political and corporate environment. Above all else, financial markets dislike uncertainty. Yet markets are also prone to over-react to events that cloud the short-term outlook. As an investor, it is important to take a step back at these times and keep an open mindset.

When we are prepared at the outset for episodes of volatility on the investing journey, we are less likely to be surprised when they happen, and more likely to react rationally. By having an open mindset and a longer-term investment perspective that accepts short-term volatility, investors can begin to take a more dispassionate view. Not only does this help with the job of staying focused on long-term investment goals, it also allows investors to begin to exploit lower prices rather than lock in losses by emotionally selling at lower prices.

2. Over the long term, equity risk is usually rewarded

Equity investors are typically rewarded for the extra risk they face – compared to, for example, sovereign bond investors – with higher average returns over the longer term. It is also important to remember that risk is not the same as volatility. Asset prices regularly deviate from their intrinsic value as markets overshoot or undershoot, so investors can expect price volatility to create opportunities. In the long term, stock prices are driven by corporate earnings and have generally outperformed other types of investment in real terms, i.e. after inflation (see Charts 4, 5, 6 and 7).

3. Market corrections can create attractive opportunities

Corrections are a normal feature of stock markets; it is normal to see more than one over the course of a bull market. A stock market correction can be a good time to invest in equities as valuations become more attractive, giving investors the potential to generate above-average returns when the market rebounds. Some of the worst historical short-term stock market losses were followed by rebounds (see Chart 1).

4. Avoid stopping and starting investments

Those who remain invested typically benefit from the long-term uptrend in stock markets. When investors try to time the market and stop-and-start their investments, they can run the risk of denting future returns by missing the best recovery days in the market and the most attractive buying opportunities that become available during periods of pessimism. Missing out on just five of the best performance days in the market can have a significant impact on longer-term returns (see Chart 2 and Table 2).

5. The benefits of regular investing stack up

Irrespective of an investor’s time horizon, it makes sense to regularly invest a certain amount of money in a fund, for example each month or quarter. This approach is known as cost averaging. While it doesn’t promise a profit or protect against a market downturn, it can help lower the average cost of fund purchases. And although regular saving during a falling market may seem counter-intuitive to investors looking to limit their losses, it is precisely at this time when some of the best investments can be made, because asset prices are lower and will benefit from any market rebound. (Investors should always review their portfolio from time to time and adjust it if needed.)

6. Diversification of investments helps to smooth returns

Asset allocation can be difficult to perfect as market cycles can be short and subject to bouts of volatility. During volatile markets, leadership can rotate quickly from one sector or market to another. Investors can spread the risk associated with specific markets or sectors by investing into different investment buckets to reduce the likelihood of concentrated losses. For example, holding a mix of ‘risk’ assets (equities, real estate and credit) and defensive assets (government and investment grade bonds, and cash) in your portfolio can help to smooth returns over time.

Investing in actively managed multi-asset funds can be a useful alternative for some investors as they provide ready-made asset level and geographic portfolio diversification. These funds are typically constructed on the basis of strategic long-term asset returns, with asset weights managed tactically according to expected conditions. Spreading investments over different countries can also help to bring down correlations within a portfolio and reduce the impact of market-specific risk.

7. Invest in quality, dividend-paying stocks for regular income

Sustainable dividends paid by high quality, cash-generative companies can be especially attractive, because the income element tends to be stable even during volatile market periods. High quality, income-paying stocks tend to be leading global brands that can weather the ups and downs of the business cycle thanks to their established market shares, strong pricing power, and resilient earnings streams. These companies typically operate in multiple regions, smoothing out the effects of patchy regional performance. This through-cycle ability to offer attractive total returns makes them a useful component of any portfolio.

8. Reinvest income to increase total returns

Reinvesting dividends can provide a considerable boost to total returns over time, thanks to the power of compound interest (see Chart 3). To achieve an attractive total return, investors need to be disciplined and patient, with time in the market perhaps the most critical yet underestimated ingredient in the winning formula. Regular dividend payments also tend to support share price stability and dividend-paying stocks can help protect against the erosive effects of inflation.

9. Don’t be swayed by sweeping sentiment

The popularity of investment themes ebbs and flows – for instance, technology has come full circle after a late 90s boom and 2000s bust. Overall sentiment to emerging markets tends to wax and wane with the commodity cycle and as economic growth slows in key economies like China. As country and sector specific risks become more prominent, investors need to take a discriminating view, since a top-down approach to emerging markets is no longer appropriate.

But there are still great opportunities for investors at the stock level, as innovative emerging companies can take advantage of supportive secular drivers like population growth and expanding middle class demand for healthcare, technology and consumer goods and services. The key point is not to allow the euphoria or undue pessimism of the market to cloud your judgement.

10. Active investment can be a very successful strategy

When volatility increases, the flexibility of active investing can be especially rewarding compared to the rigid allocations of passive investments. In particular, volatility can introduce opportunities for bottom-up stock-pickers, especially during times of market dislocation. At Fidelity, we believe strongly in active management and we have one of the largest buy-side research teams in the asset management industry to support this. Because we analyse companies from the bottom up, we are well positioned to invest when other investors might be shying away during bouts of market volatility.

Remember, too, that the stocks you do not own in a fund can be as important as the ones you do own. There are companies in every stock market that are poorly managed or which suffer from fundamentally difficult outlooks; active managers can avoid these stocks. Moreover, the value added by avoiding some of the worst stocks in the market builds over cycles and with the passage of time, making research-driven active strategies particularly appealing for long-term investors.

Looking through volatility

Historical data can provide useful context that helps investors to both look through volatility and take an unemotional, long-term approach to their investments.

These charts and tables provide compelling evidence for a long-term approach, showing, for example, why an approach of stopping and starting investments over time can run the risk of missing out on some of the best periods of returns.

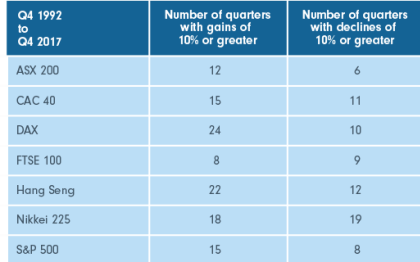

Table 1. Strongest quarters generally outnumber the weakest ones

Source: Datastream, February 2018. All calculations use local currency total returns, except for the Nikkei 225, for which the calculations are based on the price index.

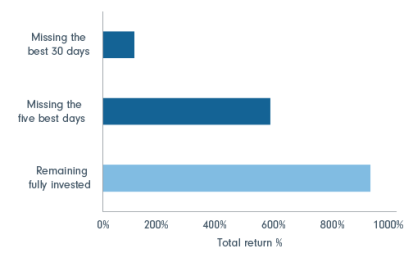

Time in the market beats timing the market

Inertia can be a positive force once the decision to invest has been made: missing the best days in the market can have a significant impact on your overall investment return.

Chart 1: Total return and impact of missing the five and 30 best days in the S&P 500 (1992-2017), US$

Source: Datastream, Fidelity International, February 2018. S&P 500 total return data from 31/12/1992 - 30/12/2017.

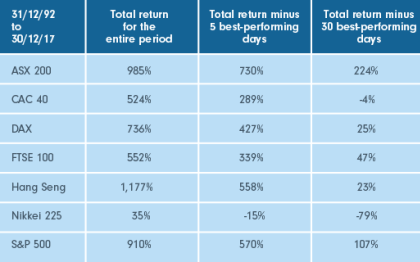

Table 2. The impact of missing five or 30 of the best-performing days over the long term

Source: Datastream, February 2018. All calculations use local currency total returns, except for the Nikkei 225, for which the calculations are based on the price index.

Table 3. The best three-year and five-year periods of return between 1992 and 2017

Source: Datastream, February 2018. All calculations use local currency total returns, except for the Nikkei 225 and the Hang Seng, for which the calculations are based on the price index. From 31/12/1992 to 31/12/2017.

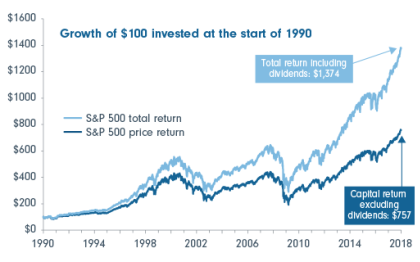

Chart 2: The power of dividend reinvesting

Source: Datastream, February 2018. Index rebased to 100 at 01/01/1990. Returns calculated for the period 01/01/1990 - 31/12/2017.

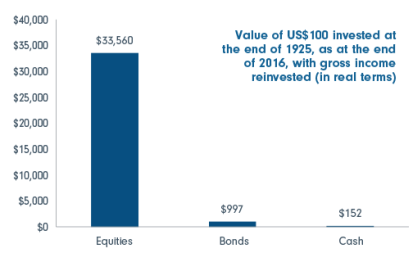

Chart 3: Equities outperform Treasuries and cash over time

Entire sample, from end-1925 to end-2016. Source: Barclays Equity Gilt Study 2017

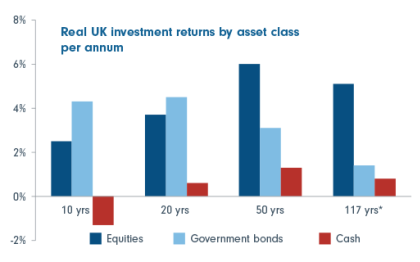

Chart 4: Equity total returns beat inflation by a wide margin

Source: Barclays Equity Gilt Study 2017

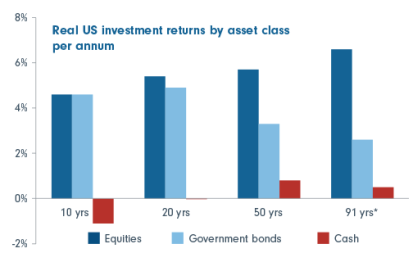

Chart 5: Equities outperform Gilts and cash over time

*Entire sample, from end-1899 to end-2016. Source: Barclays Equity Gilt Study 2017

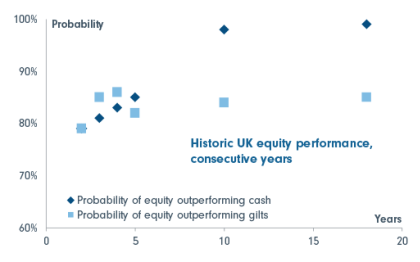

Chart 6: Probability of equity outperformance grows over time

Source: Barclays Equity Gilt Study 2017

Chart 7: ‘Three strikes and I’m out’

Source: Datastream, February 2018

One of the most serious investment implications of following the herd is that investors end up buying when prices are high and selling when prices are low.

In addition, we avoid losses as we feel the pain of a loss about twice as deeply as the happiness from a gain.

Moreover, there are two principal behavioural biases that can kick in during times of market stress, causing investors to capitulate and sell at the wrong time for the wrong reasons: herding and loss aversion. The urge to do as others are doing is a particularly powerful bias in human behaviour that has aided social development, but is not always helpful in investing.

More seriously, following the herd means that investors end up buying when prices are high and selling when prices are low. This is known as ‘chasing the market’ - a terrible investment strategy. In reality, it is typically better to do the opposite, buying when others are fearful and prices are low, and selling when other are greedy and prices are high. The best investors know this but for many of us, going against the herd feels very difficult as we have to fight our emotions.

The second bias, loss aversion, is one of the most significant behavioural biases that can affect investment. Experiments show that people take the safe option in gambles that involve gains, but take risk in gambles that involve losses, and that we feel the pain of a loss twice as deeply as the happiness from a gain.

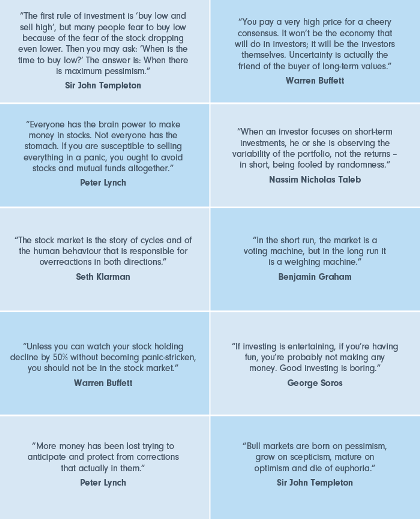

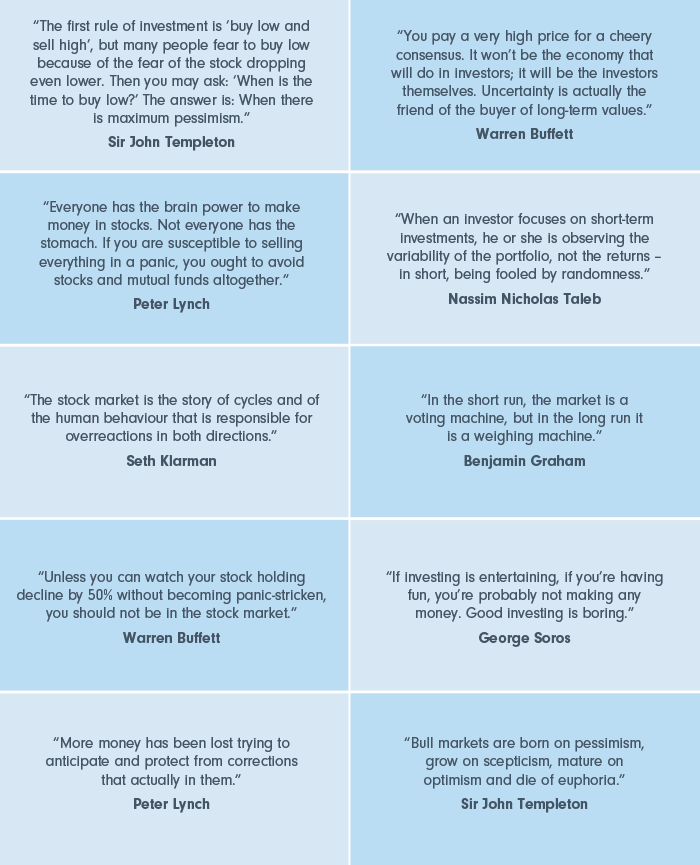

What the experts say

These quotes from some of the most successful investors illustrate how investing in stock markets can be a challenging yet rewarding venture, requiring strong research skills, a rational, dispassionate mindset, a long-term horizon and patience in equal measure.

Source : Fidelity February 2018

Reproduced with permission of Fidelity Australia. This article was originally published at https://www.fidelity.com.au/insights/investment-articles/volatility-an-investor-survival-guide/

This document has been prepared without taking into account your objectives, financial situation or needs. You should consider these matters before acting on the information. You should also consider the relevant Product Disclosure Statements (“PDS”) for any Fidelity Australia product mentioned in this document before making any decision about whether to acquire the product. The PDS can be obtained by contacting Fidelity Australia on 1800 119 270 or by downloading it from our website at www.fidelity.com.au. This document may include general commentary on market activity, sector trends or other broad-based economic or political conditions that should not be taken as investment advice. Information stated herein about specific securities is subject to change. Any reference to specific securities should not be taken as a recommendation to buy, sell or hold these securities. While the information contained in this document has been prepared with reasonable care, no responsibility or liability is accepted for any errors or omissions or misstatements however caused. This document is intended as general information only. The document may not be reproduced or transmitted without prior written permission of Fidelity Australia. The issuer of Fidelity Australia’s managed investment schemes is FIL Responsible Entity (Australia) Limited ABN 33 148 059 009. Reference to ($) are in Australian dollars unless stated otherwise.

© 2018. FIL Responsible Entity (Australia) Limited.

Important:

This provides general information and hasn’t taken your circumstances into account. It’s important to consider your particular circumstances before deciding what’s right for you. Any information provided by the author detailed above is separate and external to our business and our Licensee. Neither our business, nor our Licensee take any responsibility for any action or any service provided by the author.

Any links have been provided with permission for information purposes only and will take you to external websites, which are not connected to our company in any way. Note: Our company does not endorse and is not responsible for the accuracy of the contents/information contained within the linked site(s) accessible from this page.

{kind=link}